Though investment in food technology has slowed in line with the rest of the venture capital world, the industry recently achieved some milestones that suggest the sector and the government are moving into alignment.

In fact, some investors feel that 2023 will be the year when alternative seafood companies and products make notable strides.

More than $178 million was pumped into alternative seafood in the first half of 2022, and the market’s value is poised to reach $1.6 billion over the next 10 years. One of the sector’s biggest investments was Wildtype, which raised $100 million in a Series B round for its “sushi-grade” cultured salmon.

If this momentum held in the past six months, funding into the sector would meet or exceed the $306 million invested in all of 2021, despite the slowdown last year.

“Investment has been growing steadily, and we expect this to continue,” said Christian Lim, managing partner at SWEN Capital Partners’ Blue Ocean. “We see the alternative seafood industry achieving key technical and economic milestones faster than the alternative meat space, which indicates a potential for continued acceleration,” he said.

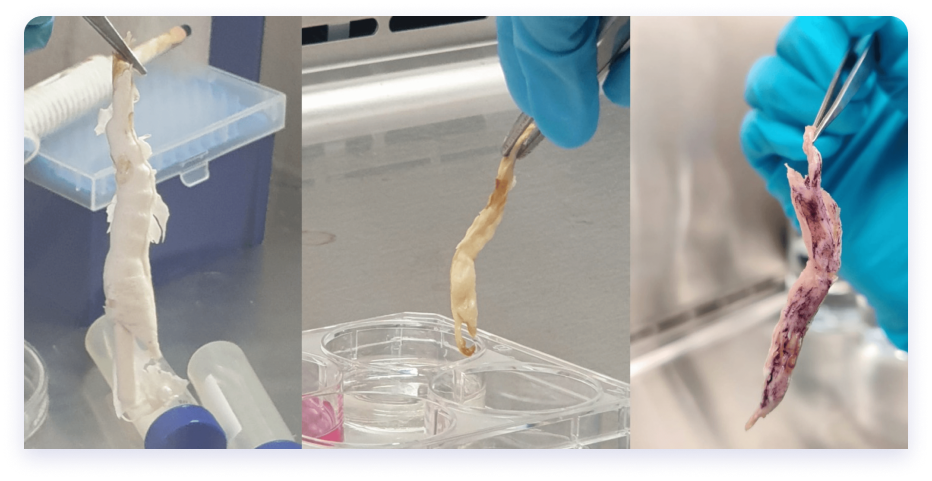

Many companies say they are in this for the sustainability factor, and even with the initial blessing from the FDA to Upside Foods for its cultivated chicken-making process, the focus is on getting these alternative foods close to the scalability and cost of traditional meat.

“The cultivated seafood industry is beyond needing to solve for the technology — the technology is there and it continues to improve with every iteration,” said Kate Danaher, managing director, S2G Ventures. “Now we need to think about brand-building, labeling, consumer education, scaling production, and developing and improving the supply chain and inputs that will support a scalable industry.”

Like other plant-based, cultured and fermented food companies, alternative seafood companies also must figure out the best way to get people to not only give their products a try but to ask for seconds.

As we kick off 2023, investors say regulation will help alternative seafood make additional strides, and they are optimistic that traction will be found. Read on to find out how active investors are thinking about alternative seafood, where they see growth, what they are keeping their eye on and more.

We spoke with:

- Kate Danaher, managing director, S2G Ventures Oceans and Seafood

- Friederike Grosse-Holz, director, Blue Horizon

- Christian Lim, managing director, SWEN Capital Partners’ Blue Ocean

- Amy Novogratz, co-founder and managing partner, Aqua-Spark

Kate Danaher, managing director, S2G Ventures Oceans and Seafood

What will it take for the alternative seafood industry to have its first unicorn? Do you think 2023 is the year for it? Which companies do you think are close to achieving this milestone?

I do not expect the first alternative seafood unicorn to happen in 2023. The first goal we should all be focused on is demonstration of repeated production runs at viable price points.

Cultivated protein companies have made tremendous progress in the development of their products, but the big hurdle is getting a product of consistent quality and cost to the market.

To date, we have seen big dollars flowing to support the first wave of cultivated protein products, including in seafood. To achieve the step up in valuations that will eventually lead to a unicorn, companies will have to demonstrate a quality product with margins that fit within a viable business model at scale.

There have been some strides in the U.S. toward approving the process for producing alternative protein. How can founders work with regulators and investors to bring more proof-of-concept projects to fruition?

Many constituencies need to be “won over” to mitigate the headwinds that cultivated protein is likely to meet as it goes to market, such as industry groups, consumer groups and regulators.

Startup founders can support industry growth, commercialization and acceptance by building bridges with industry groups to show that cultivated seafood can be complementary to wild and farmed seafood.

Additionally, they should provide transparency into the production process to win over consumer groups and join an association, such as AMPS or Good Food Institute, who are doing important regulatory work on behalf of the industry.

Depending on whom you ask, mainstream production of alternative proteins, like beef, chicken and pork, is still years away. How can the alternative seafood industry achieve this faster?

I feel confident that alternative protein products will be available for purchase in the U.S. in the next 12 months, both cultivated seafood and other animal proteins. But for the foreseeable future, that product will be niche, premium and in limited production. Once production capacity constraints are resolved and costs come down, I expect these products to be as widely available as their animal protein counterparts.

One area where seafood may have an advantage in speed to market is related to regulation, given the FDA has sole jurisdiction over alternative proteins whereas the USDA and FDA share jurisdiction over animal protein.

In addition, seafood has a higher price point and its muscle structure is simpler in comparison to other animal proteins, making it more straightforward to grow a product that more easily replicates wild/farmed species.

Many alternative seafood startups aim to solve for the climate crisis as well, but this industry has unique challenges such as cost and appealing to consumers. What will be key in helping companies produce sustainable products at scale?

For cultivated seafood, the technology is there and it continues to improve with every iteration. Now we need to think about brand building, labeling, consumer education, scaling production, and developing and improving the supply chain and inputs that will support a scalable industry.

If these products can be more affordable and meet consumer expectations, they can achieve impact at scale — for the animal through less wild fishing, for humans by delivering a seafood product with no toxins or microplastics and for the environment through less waste.

Additionally, consumer education will be key. This, in part, includes driving awareness around the true cost of our food beyond what we pay in the grocery store. Consumers are becoming more aware of the externalities and factoring that into their purchasing decisions, but there is much more work to be done in that respect.

What does the future look like for investment in this space? Which areas are you highlighting as future growth indicators?

The good news is that cellular seafood products have reached a stage where they are approaching readiness to go to market from a regulatory, taste and performance perspective.

Cellular seafood companies are making amazing advancements in reducing the price and nearing the stage where they are ready for growth capital to scale the business. I expect to see more innovation and investment into the advancement of consumer experience and 3D structures.

What is needed to attract more institutional investment for later-stage funding to help scale the market?

I fully expect cellular seafood companies to be in a sold-out position in the future, because there is demand from a large early-adopter consumer segment. The next wave of investments will be into infrastructure and companies that build adjacent inputs to outsource parts of the supply chain.

We have strong indications that FDA clearance is coming, and that will tick a big box for institutional and later-stage investors. Once this is behind us, it will be about who is in the market showing traction and producing a product at a price point that makes a compelling business case.